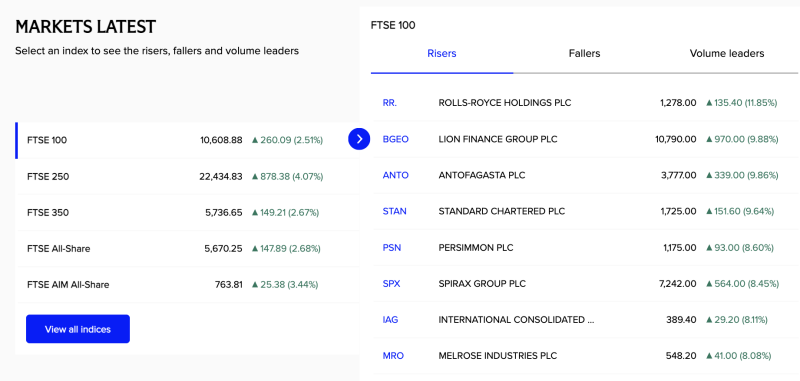

London markets saw a clear travel-led risk-on rotation, with IAG (International Consolidated Airlines Group) emerging as one of the FTSE’s top volume leaders after surging 8.11% to 389.40. The scale of the move, combined with its heavy turnover profile, suggests this was more than a stock-specific spike—it points to institutional positioning into the broader travel, leisure, and reopening basket.

The strength in IAG is significant because airline heavyweights rarely move more than 8% in a single session without a wider sector trigger. Investors appear to be pricing in stronger summer booking visibility, resilient premium route demand, and improving margin expectations as fuel-cost volatility stabilises. In UK markets, such moves typically ripple into related counters including easyJet, Wizz Air, airport retail names, hotel operators, and aerospace-linked plays such as Rolls-Royce, turning the rally into a broader cyclical sector story rather than a single-stock event.

The bigger market takeaway is that travel stocks are once again acting as confidence proxies for discretionary spending and cross-border mobility trends. When a large-cap name like IAG leads FTSE volumes, it often reflects rising conviction around consumer resilience, international traffic recovery, and better earnings visibility for leisure-linked businesses heading into the summer season.